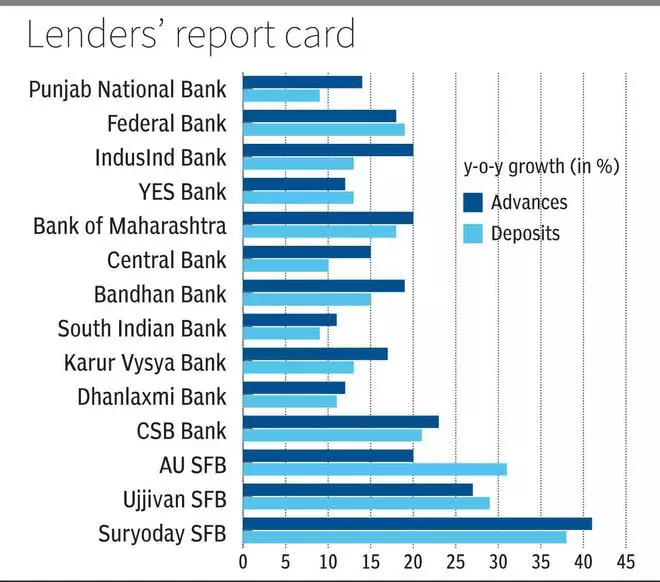

MUMBAI Banks, both public sector and private, continued to post robust double-digit loan growth of 11-23 per cent y-o-y in Q3 FY24, as per provisional figures declared by the lenders for the quarter.

Credit growth for banks such as YES Bank, South Indian Bank and Dhanlaxmi Bank was at the lower end of 11-12 per cent whereas for lenders such as IndusInd Bank, Bank of Maharashtra and CSB Bank was at the higher end of 20-23 per cent. Growth for small finance banks was over 20 per cent given their small base with Suryoday SFB posting loan growth of 41 per cent on year.

NBFCs such as Bajaj Finance and Mahindra Finance too posted strong credit growth for the quarter, with their assets under management rising by 35 per cent and 25 per cent, respectively, on year. Poonawalla Fincorp, with a smaller asset base, posted a growth of 57 per cent y-o-y.

- Also read: Indian banks have closed 25 per cent of their foreign branches since FY19

Deposit growth for banks remained steady in the reporting quarter but continued to lag loan growth barring for Federal Bank and YES Bank, which saw slightly higher deposit growth. Rise in deposits for Punjab National Bank and South Indian Bank fell below the double-digit mark at 9 per cent.

Small finance banks saw accelerated rise in deposits posting growth of 29-38 per cent, likely on the back of higher interest rates being offered by these banks on savings accounts and fixed deposits to hasten deposit accretion and build their liability profiles.

Sequentially, loan growth for banks was in the range of 2-8 per cent, whereas deposit growth was at 1-8 per cent. Here too, deposit growth lagged loan growth for most major banks.

CASA deposits

Much of the deposit growth during the quarter was led by fixed and bulk deposits as CASA (current and savings accounts) deposits remained under pressure. CASA deposits have been slowing down for most lenders over the past several quarters as investors are shifting to higher yielding investment avenues. This has increased banks’ reliance on other forms of deposits, including substantially increasing rates on term deposits. This led to RBI to recently cautioning banks against over-reliance on bulk deposits.

CASA ratios for banks, which have declared their provisional numbers, fell to 25.3-50.2 per cent from 26.2-52.5 per cent in the year ago period. Suryoday SFB was the outlier seeing an increase in its CASA ratio to 18.5 per cent from 14.1 per cent, even as its share of CASA deposits remain much below the industry average.