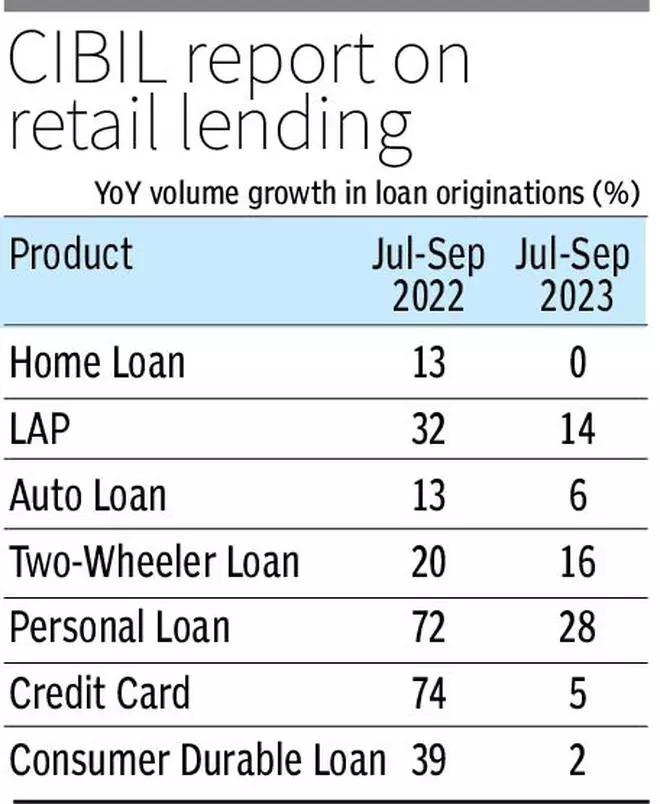

Retail lending witnessed moderation in growth during the quarter ended September 2023 as financial institutions tightened the supply of credit, especially on consumption-led products such as credit cards, consumer durable loans, and personal loans.

Credit performance, as measured by balance-level delinquencies, improved across most products other than credit cards and personal loans, according to TransUnion CIBIL’s Credit Market Indicator (CMI) report for September 2023.

The report showed an on-year decline in growth rate of overall originations, resulting in a marginal decline in the CMI supply index from 98 in September 2022 to 95 in September 2023. Growth of consumption-led credit products moderated in the quarter ending September 2023, including personal loans whereas that on home loans was stagnant.

While home loans grew 9 per cent in terms of value, the volume of loans sanctioned was flat on year. This was led by a 4 per cent decline in origination of low-value home loans of less ₹35 lakh, which form 76 per cent of originations. Home loans of ₹75 lakh and above, which form 7 per cent of the origination volume, grew by 23 per cent on year, reflecting the upward trend in property prices in 2023.

The number of loans disbursed by private banks grew only 1 per cent on year, whereas those by PSU banks rose by 17 per cent. In terms of the amount of loans, private bank disbursements were up 19 per cent and PSU bank sanctions by 17 per cent. Personal loans portfolio grew 27 per cent on year, but its share in retail credit portfolio grew by a marginal 20 bps.

New customers

Demand for semi-urban and rural customers rose 3 per cent on year, but from younger and new to credit (NTC) customers fell 1 per cent, whereas from prime customers fell by 2 per cent from September 2022. Share of NTC consumers in originations dropped from 17 per cent in September 2022 to 14 per cent, resulting in a decrease in share of NTC origination volumes from 12 per cent to 10 per cent.

Overall balance-level serious delinquencies (90 days or more past due) continued to improve across product categories, except for marginal deterioration in credit cards and personal loans.

“This stability now provides a strong bedrock for driving balanced and sustained credit growth across products. Intensive monitoring of portfolios, while also finding and funding the lower-risk consumers who deserve financial opportunities for fulfilling their aspirations, can set India’s credit industry on the path for long-term growth,” said MD and CEO Rajesh Kumar.